![]()

PF1 PDF Pass Leader, PF1 Latest Real Test

Valid PF1 Test Answers & PF1 Exam PDF

NEW QUESTION # 14

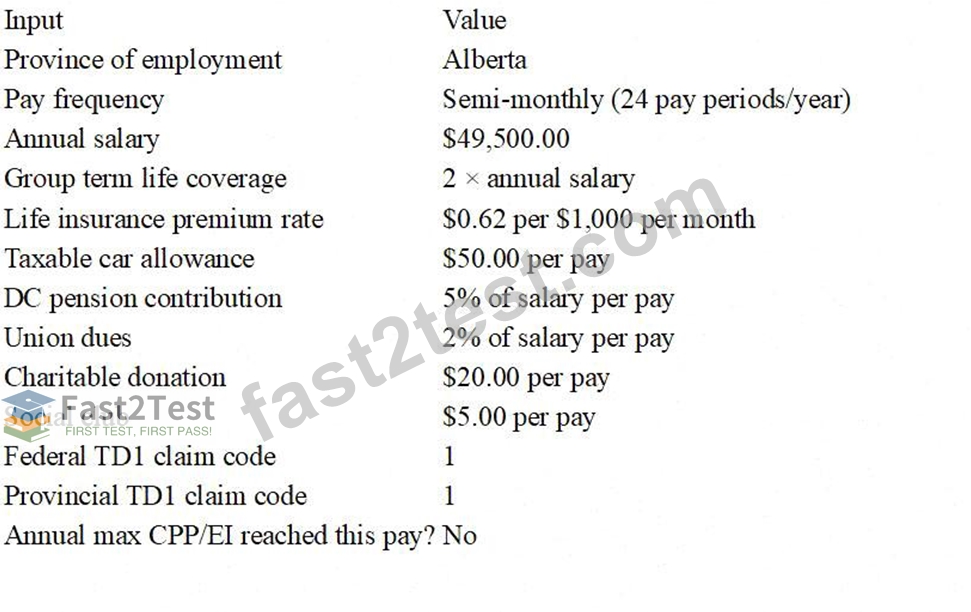

PF1 Exam - Net Pay Calculation (Template Worksheet)

Scenario

Diane Lemay works for Monarch Construction in Alberta and earns an annual salary of $49,500.00, paid on a semi-monthly basis.

The company provides its employees with group term life insurance coverage of two times annual salary and pays a monthly premium of $0.62 per $1,000.00 of coverage.

Diane uses her car to meet with clients on company business and receives a taxable car allowance of $50.00 per pay.

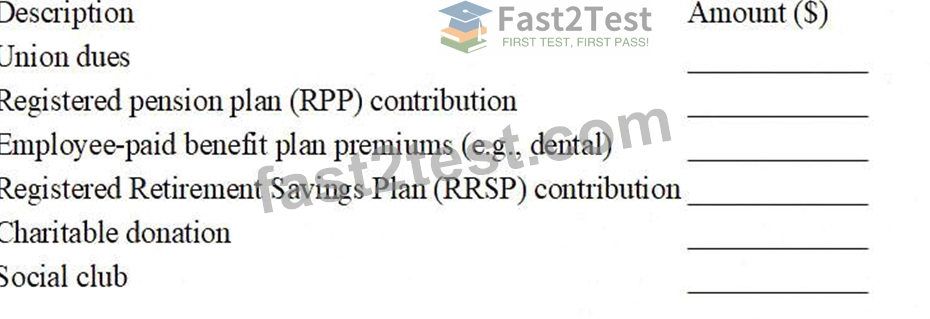

The company has a defined contribution pension plan to which Diane contributes 5% of her salary each pay.

Diane also contributes $20.00 to United Way and has $5.00 deducted for her social club membership each pay. She belongs to a union and pays 2% of her salary in union dues per pay period.

Diane's federal and provincial TD1 claim codes are 1. She will not reach the first Canada Pension Plan or Employment Insurance annual maximums this pay period.

Required: Calculate the employee's net pay, following the order of the steps in the net pay template.

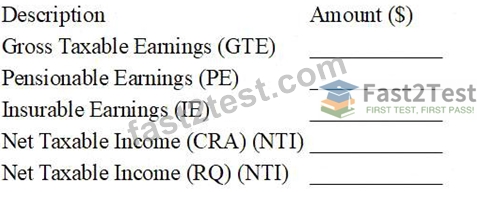

EXHIBIT A - Net Pay Template (Fill in all blanks)

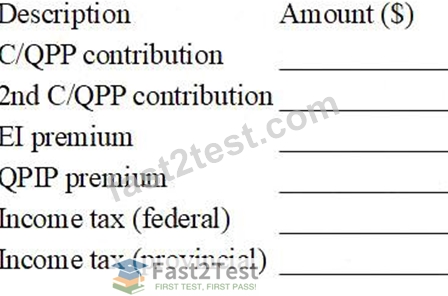

STATUTORY DEDUCTIONS

OTHER DEDUCTIONS

Given Data (Reference)

Step 1 - Calculate the employee's gross taxable earnings (GTE) for this pay.

[ _________________________________ ]

Step 2 - Calculate the pensionable earnings (PE).

[ _________________________________ ]

Step 3 - Calculate the insurable earnings (IE).

[ _________________________________ ]

Step 4 - Calculate the net taxable income (CRA) (NTI).

[ _________________________________ ]

Step 5 - Calculate the net taxable income (RQ) (NTI).

[ _________________________________ ]

Step 6 - Calculate Diane's Canada Pension Plan contribution.

[ _________________________________ ]

Step 7 - Calculate Diane's Employment Insurance premium.

[ _________________________________ ]

Step 8 - Calculate Diane's Quebec Parental Insurance Plan premium.

[ _________________________________ ]

Step 9 - Determine Diane's federal income tax.

[ _________________________________ ]

Step 10 - Determine Diane's provincial income tax.

[ _________________________________ ]

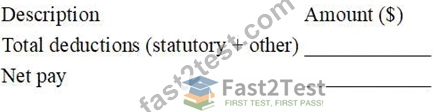

Step 11 - Calculate Diane's total deductions (statutory + other).

[ _________________________________ ]

Step 12 - Calculate Diane's net pay.

[ _________________________________ ]

Answer:

Explanation:

See the Explanation part for answer for each step.

Explanation:

Step 1 - Gross Taxable Earnings (GTE)

Salary per pay: 49,500 ÷ 24 = $2,062.50

Taxable car allowance: $50.00

Group term life taxable benefit:

Coverage = 2 × 49,500 = 99,000

Monthly premium = (99,000 ÷ 1,000) × 0.62 = 99 × 0.62 = 61.38

Semi-monthly benefit = 61.38 ÷ 2 = $30.69

GTE = $2,143.19

Step 2 - Pensionable Earnings (PE)

PE = $2,112.50 (2,062.50 + 50.00)

Step 3 - Insurable Earnings (IE)

IE = $2,112.50

Step 4 - Net Taxable Income (CRA) (NTI)

RPP = 5% × 2,062.50 = $103.13

Union dues = 2% × 2,062.50 = $41.25

NTI (CRA) = 2,143.19 # 103.13 # 41.25 = $1,998.81

Step 5 - Net Taxable Income (RQ)

$0.00

Step 6 - CPP (base CPP)

Period exemption = 3,500 ÷ 24 = $145.83

Contributory = 2,112.50 # 145.83 = $1,966.67

CPP = 1,966.67 × 5.95% = $117.02

CPP = $117.02

Step 6B - 2nd CPP (CPP2)

CPP2 = $0.00

Step 7 - EI premium

EI = 2,112.50 × 1.63% = $34.43

EI = $34.43

Step 8 - QPIP

$0.00

Step 9 - Federal income tax (CC1, semi-monthly)

$156.10

Step 10 - Alberta income tax (CC1, semi-monthly)

$73.20

Step 11 - Total deductions

Statutory: 117.02 + 34.43 + 156.10 + 73.20 = $380.75

Other: RPP 103.13 + Union 41.25 + United Way 20.00 + Social club 5.00 = $169.38 Total deductions = $550.13 Step 12 - Net pay Cash pay (salary + car allowance) = 2,062.50 + 50.00 = $2,112.50 Net pay = 2,112.50 # 550.13 = $1,562.37

NEW QUESTION # 15

Which pension plan requires the services of an actuary to study and forecast future needs of the plan to ensure the plan remains sufficiently funded to provide employees with their retirement benefits?

- A. Defined benefit pension plan

- B. Registered Retirement Savings Plan

- C. All of the above

- D. Defined contribution pension plan

Answer: A

NEW QUESTION # 16

Dollar values attributed to something the employer has either provided to an employee or paid for on an employee's behalf are:

- A. Expense reimbursements

- B. Benefits

- C. Earnings

- D. Allowances

Answer: B

Explanation:

The CRA defines a benefit as something the employee receives when the employer pays for or gives something that is personal in nature (a good or service), either directly to the employee or through a third party. CRA's T4130 guide describes a benefit as a good or service you give (or arrange for) such as free use of employer property, and it is the value of that benefit that may need to be included in the employee's income if taxable.

This matches the wording in the question: "dollar values attributed to something the employer has either provided...or paid for...on an employee's behalf." By contrast, earnings are pay for work performed (salary, wages, commissions). Allowances are fixed amounts paid to help cover anticipated expenses without receipts (often taxable unless an exception applies). Expense reimbursements repay actual business expenses (typically supported by receipts) and are generally not treated as earnings.

So the correct classification is Benefits.

NEW QUESTION # 17

Paula is granted a pay increase. The paperwork informing the payroll department of the pay increase is two pay periods late. What method would be used to calculate income taxes on the separate retroactive payment?

- A. Bonus tax method

- B. Tax table method

- C. Retroactive tax method

- D. Lump-sum tax method

Answer: C

Explanation:

A payment made to "catch up" wages because a pay increase was processed late is a retroactive payment. The CRA provides different income tax calculation approaches depending on the payment type and specifically lists "Retroactive payments" as its own category, separate from regular tax-table calculations, lump-sum, and bonus/irregular methods.

For bonuses and retroactive pay increases, the CRA also points employers to the Payroll Deductions Online Calculator (PDOC) to calculate CPP, EI, and income tax correctly, which aligns with using the appropriate CRA method for retroactive amounts.

Because this situation is explicitly a retroactive adjustment (two pay periods late), the correct choice is the Retroactive tax method (option C), not the bonus/irregular method, not the lump-sum method, and not the regular tax tables.

NEW QUESTION # 18

An employee who lives in Ontario and reports to work at a permanent establishment of the employer in Quebec will have income tax deducted based on which province?

- A. Employee's choice

- B. Ontario & Quebec

- C. Ontario

- D. Quebec

Answer: D

Explanation:

For payroll deductions, the key concept is the employee's province of employment (POE)-not where they live. The CRA states that the POE is determined primarily by the employer's establishment where the employee "reports for work." If an employee reports for work at an employer's establishment located in Quebec, then the POE is Quebec, even if the employee's province of residence is Ontario.

This matters because Quebec has distinct payroll requirements. The CRA notes that when the POE is Quebec, employers must apply Quebec-based payroll rules, including deducting Quebec Pension Plan (QPP) contributions instead of CPP, and deducting Quebec parental insurance plan (QPIP) premiums, along with Quebec provincial income tax withholding.

In practice, payroll must set up the employee using Quebec as the POE and ensure stakeholders (HR, finance, the employee) understand why deductions may differ from Ontario residents working in Ontario. Any over

/under-withholding due to POE vs. residence is typically reconciled when the employee files their personal tax return.

NEW QUESTION # 19

The Canada Revenue Agency form that is completed to allow a commissioned employee to claim non- reimbursed expenses at source is a:

- A. T777

- B. TP-1015.R.13.1-V

- C. TD1

- D. TD1X

Answer: D

Explanation:

The CRA form used to adjust payroll income tax withholdings at source for employees who earn commission income and have commission expenses is Form TD1X - Statement of Commission Income and Expenses for Payroll Tax Deductions. The CRA explains that an employee completes TD1X if they receive commission income (or salary plus commission) and want the employer to adjust tax deductions to take commission expenses into account.

This is different from:

TD1, which is the Personal Tax Credits Return used to claim basic/personal credits and determine standard withholding (not commission-expense adjustments).

T777, which is used to claim employment expenses on the employee's personal tax return (not to reduce payroll withholding at source).

TP-1015.R.13.1-V, which is a Quebec form used to request a reduction of Quebec income tax withholding in specific situations (not the CRA commission-expense at-source form).

Operationally, payroll should keep the TD1X on file and apply it to income tax withholding calculations until the employee updates or replaces it.

NEW QUESTION # 20

Anthony earns $750.00 per week. He has a cash taxable benefit of $25.00 per week. Anthony is exempt from CPP contributions. Calculate the net taxable income for the week.

Answer:

Explanation:

$775.00

Explanation:

"Net taxable income" for payroll withholding purposes is the amount of income on which income tax is calculated for the pay period. It generally starts with the employee's gross taxable earnings for the period (regular wages plus any taxable benefits/allowances that must be included in income), then subtracts only those deductions that are deductible for tax at source (for example, certain registered pension plan contributions, union dues, etc., if applicable). A cash taxable benefit is treated like additional remuneration and is included in taxable income. (canada.ca) Here, Anthony's weekly taxable earnings are:

$750.00 wages + $25.00 cash taxable benefit = $775.00.

Being exempt from CPP contributions affects whether CPP is deducted, but CPP is not a "net taxable income" subtraction in this question (and in any case, no CPP is being deducted). The question also does not mention any other tax-deductible payroll deductions (like RPP contributions), so there is nothing to subtract from taxable earnings.

Therefore, Anthony's net taxable income for the week is $775.00.

NEW QUESTION # 21

When is the government-prescribed rate of interest set?

- A. Each calendar quarter

- B. Annually

- C. Semi-annually

- D. The first of each month

Answer: A

Explanation:

The CRA's prescribed interest rates are established for specific periods labelled by calendar quarter (for example, "first calendar quarter 2026"), and CRA publishes the rate schedule by quarter.

This prescribed rate is used in multiple tax contexts, including calculating taxable benefits on certain interest- free or low-interest employee/shareholder loans, and it also relates to interest charged/paid by the CRA on overdue amounts and overpayments (with different rates for different situations).

Because CRA's publication is organized and effective by quarter (e.g., Jan 1-Mar 31; Apr 1-Jun 30; Jul 1- Sep 30; Oct 1-Dec 31), the correct answer is each calendar quarter (option D), not monthly, semi-annual, or annual.

NEW QUESTION # 22

An employee has the use of a company-leased vehicle for both business and personal use. This is an example of:

- A. An allowance

- B. An earning

- C. An expense reimbursement

- D. A benefit

Answer: D

Explanation:

This is a benefit because the employer is providing access to an automobile (leased by the employer) that the employee can use for personal driving as well as business. The CRA explains that when an employer-owned or employer-leased automobile is made available for personal use, the employee receives a taxable automobile benefit, generally made up of a standby charge (availability of the vehicle) and potentially an operating expense benefit (if the employer pays operating costs and the employee has personal kilometres).

It is not an allowance (which is typically a cash amount given to the employee), and it is not an expense reimbursement (repayment of employee-incurred business expenses). It is also not an earning (pay for work performed). Payroll's role is to track availability days/months, business vs personal kilometres, any employee reimbursements, apply the CRA calculation methods, and report the taxable benefit on the employee's information slip with the correct taxable benefit treatment.

NEW QUESTION # 23

Steve is physically disabled and his employer pays for his parking spot. This is considered:

- A. A non-cash taxable benefit

- B. A taxable allowance

- C. A cash taxable benefit

- D. None of the above

Answer: D

Explanation:

Employer-provided parking is often a taxable benefit, generally valued at the fair market value of the parking spot. However, the CRA provides a specific exception for employees with disabilities. CRA guidance on employer-provided parking states that if your employee has a disability, the parking benefit is generally not taxable, including situations involving a severe and prolonged mobility impairment or blindness.

In Steve's case, the fact pattern explicitly says he is physically disabled and the employer pays for his parking.

Under CRA's general rule for disability-related parking, this would generally not be included in income as a taxable benefit, meaning it is not a taxable allowance and not a taxable benefit (cash or non-cash) for payroll purposes.

Payroll should still document why the parking is being treated as non-taxable (for example, disability-related need) and ensure the treatment aligns with CRA guidance if questioned. If the facts were different (non- disability parking or preferential parking provided to employees generally), the taxable benefit rules would usually apply.

NEW QUESTION # 24

Elodie is paid her commissions together with her bi-weekly salary of $1,000.00. This pay period her commissions are $4,300.00. Calculate her Quebec Pension Plan (QPP) contribution for this pay period.

Answer:

Explanation:

$325.42

Explanation:

Because Elodie is subject to QPP, her pensionable earnings for the pay period include both salary and commissions (both are pensionable employment earnings, assuming no exemptions apply). First, determine total pensionable earnings for the bi-weekly pay:

$1,000.00 + $4,300.00 = $5,300.00.

For 2026, Revenu Quebec shows the QPP basic exemption is $3,500 annually and the (employee) QPP contribution rate on earnings up to the maximum pensionable earnings is 6.30%.

Payroll applies the exemption per pay period. For bi-weekly pay (26 pay periods):

$3,500 ÷ 26 = $134.62 (rounded to cents).

Pensionable earnings subject to QPP this pay:

$5,300.00 # $134.62 = $5,165.38.

QPP contribution:

$5,165.38 × 6.30% = $5,165.38 × 0.063 = $325.41894, which rounds to $325.42.

NEW QUESTION # 25

Michael is an employee in Alberta who is paid bi-weekly and earns $1,600.00 per pay period. He has a taxable meal allowance of $30.00 per pay period. His federal and provincial TD1s on file show a claim code

2. Michael already reached the annual maximum first and second Canada Pension Plan (CPP) contributions before this pay. Calculate his total federal and provincial income taxes.

Answer:

Explanation:

(total federal + Alberta tax): $173.48

Explanation:

Taxable gross for the period = $1,600.00 + $30.00 = $1,630.00 (a taxable allowance is included in income for tax withholding).

Using CRA T4032-AB (Biweekly, 26 pay periods) with claim code 2:

Federal tax at pay $1,630 falls in the $1,619-$1,635 range # CC2 = $107.35.

Alberta provincial tax at pay $1,630 falls in the $1,628-$1,644 range # CC2 = $46.55.

Subtotal tax from the tables = $107.35 + $46.55 = $153.90.

CRA notes these tax tables build in the tax credits for CPP/EI, so when CPP is not deducted (because annual max already reached), you must increase tax withholding accordingly.

CPP that would have been deducted this pay (using CRA rates/YBE):

Pensionable = $1,630 # ($3,500/26 = $134.62) = $1,495.38; CPP (4.95% + 1.00% = 5.95%) = $88.98.

Add back missing credits: Federal 14% × 88.98 = $12.46; Alberta 8% × 88.98 = $7.12 # total $19.58.

Final total tax = $153.90 + $19.58 = $173.48.

NEW QUESTION # 26

A retiring allowance includes:

- A. Vacation pay

- B. Legislated wages in lieu of notice in Quebec

- C. None of the above

- D. Accumulated overtime

- E. Bonus or incentive pay

Answer: C

Explanation:

The CRA defines a retiring allowance (also called severance pay) as an amount paid when or after an employee retires or loses their job, in recognition of long service or for the loss of employment.

However, the CRA is also explicit about what a retiring allowance does not include. It does not include

"salary, wages, bonuses, [or] overtime," which rules out bonus/incentive pay and accumulated overtime in the options. It also does not include "payments for accumulated vacation leave not taken," which rules out vacation pay as a retiring allowance. Finally, it does not include wages in lieu of termination notice, which rules out wages in lieu (including legislated notice pay) as a retiring allowance.

Because every listed item is specifically excluded by CRA guidance, the correct answer is None of the above (E).

NEW QUESTION # 27

Raminder was hired in January 1997. He was fully vested in the organization's pension plan at the time he received the retiring allowance. His employment was terminated on May 1, 2006 and he was paid a

$10,000.00 retiring allowance. Calculate the eligible portion of the retiring allowance.

- A. $2,000.00

- B. None of the retiring allowance is eligible

- C. $10,000.00

- D. $7,500.00

Answer: B

Explanation:

The "eligible portion" of a retiring allowance (the part that may be transferred directly to an RRSP/RPP on a tax-deferred basis without using regular RRSP room) is based on years of service before 1996 (and potentially an additional amount for certain pre-1989 years). CRA explains that the eligible part is: $2,000 for each year or part-year of service before 1996, plus an additional $1,500 for each year or part-year of service before 1989 only if no employer-funded pension/DPSP benefits for those years were vested (or previously paid out).

Raminder was hired in January 1997, so he has zero years (or part-years) of service before 1996, and therefore he has no base eligible amount under the $2,000-per-year rule. Because he also has no pre-1989 service, the additional $1,500-per-year rule does not apply either.

So, the eligible portion is $0, meaning none of the $10,000 retiring allowance is eligible (option D).

NEW QUESTION # 28

In which province or territory is the employer-paid premium for private health insurance coverage that includes dental and prescription coverage considered to be a non-cash taxable benefit?

- A. British Columbia

- B. Ontario

- C. Quebec

- D. Yukon

Answer: C

Explanation:

In Quebec, employer-paid premiums (contributions) to a group insurance plan, including a private health services plan (which commonly covers items like dental and prescription drugs), are treated as a taxable benefit for the employee for Quebec purposes. Revenu Quebec explicitly states that contributions (premiums) an employer pays under a group insurance plan for coverage received by an employee constitute a taxable benefit.

Because the employer is paying the premium directly to the insurer (the employee receives coverage rather than cash), this is treated as a non-cash taxable benefit in payroll classification terms. The payroll impact is that this taxable benefit must be included in the employee's Quebec taxable income and reported on the RL-1 (and handled according to Quebec source deduction rules).

Outside Quebec, employer-paid health/dental plan premiums are generally not treated the same way for provincial taxable benefit purposes, which is why the correct answer among the options is Quebec.

NEW QUESTION # 29

Bonus and incentive pays are subject to which statutory deductions?

- A. Canada/Quebec Pension Plan contributions, Employment Insurance premiums and income taxes

- B. Canada/Quebec Pension Plan contributions, Quebec Parental Insurance Plan premiums, income taxes and Northwest Territories/Nunavut payroll taxes

- C. Employment Insurance and Quebec Parental Insurance Plan premiums and Northwest Territories

/Nunavut payroll taxes - D. Canada/Quebec Pension Plan contributions, Employment Insurance and Quebec Parental Insurance Plan premiums, income taxes and Northwest Territories/Nunavut payroll taxes

Answer: D

Explanation:

Bonuses and incentives are treated as taxable remuneration, so they are generally subject to the same core statutory deductions as regular earnings: CPP/QPP, EI, and income tax (and in Quebec, QPIP also applies when the remuneration is subject to EI). The CRA specifically notes that you must deduct EI premiums from bonuses/retroactive pay (up to the annual maximum), and the CRA's guidance for bonuses/irregular amounts uses tools (PDOC/formulas) that calculate CPP contributions, EI premiums, and income tax on these payments.

In Quebec payroll, remuneration that is subject to EI premiums is generally also subject to QPIP premiums, so bonuses/incentives that are EI-insurable are typically QPIP-insurable as well.

In the Northwest Territories and Nunavut, there is also a statutory territorial payroll tax that employers must withhold/remit where applicable, and the NWT guidance explicitly lists bonuses as part of employment income subject to payroll tax.

NEW QUESTION # 30

Jasmine works for a Saskatchewan employer and earns $500.00 weekly. Calculate her Employment Insurance (EI) premium.

Answer:

Explanation:

$8.15 (employee EI premium for the week)

Explanation:

For employees whose province of employment is outside Quebec (including Saskatchewan), EI premiums are calculated by multiplying the employee's insurable earnings by the employee EI premium rate for the year, up to the annual maximum insurable earnings. For 2026, the employee EI premium rate outside Quebec is $1.63 per $100 of insurable earnings (which is 1.63%).

Jasmine earns $500.00 weekly and (based on the question) we assume all earnings are insurable and she has not reached the annual maximum. Her EI premium is:

$500.00 × 1.63% = $500.00 × 0.0163 = $8.15.

This amount is deducted from the employee's pay and later remitted to the CRA as part of the employer's regular payroll remittance. The maximum insurable earnings for 2026 is $68,900, but at $500 per week she would only hit the maximum later in the year (if at all), so the weekly premium calculation above applies.

NEW QUESTION # 31

......

PF1 Dumps Ensure Your Passing: https://www.fast2test.com/PF1-premium-file.html

PF1 exam dumps and online Test Engine: https://drive.google.com/open?id=1LNCfkaUR_Gx1CHP3QU54aXFlJbC_a6kC